Short-term employment

What is short-term employment?

Short-term employment, also known as KFB, describes a special type of employment in which the maximum permitted duration of work within a calendar year is limited to a maximum of 3 months or a total of 70 working days. This form of employment is often used for short-term project assignments or seasonal work.

These limits are often referred to as the 70-day rule or the 3-month rule. The employer(s) must ensure that an employee does not exceed a total of 70 working days in a calendar year. These are to be counted independently of the employer. If an employee has several short-term jobs in a calendar year, the working days must be added together.

The advantages of short-term employment include the fact that no or very low social security contributions are payable.

What taxes are due for short-term employment?

No social security contributions have to be paid for short-term employment. Neither employers nor employees are obliged to pay contributions to pension insurance, long-term care insurance, unemployment insurance, health insurance or accident insurance.

This has advantages for both the employee and the employer. The employee receives more net from his gross payout. The employer has lower personnel costs. This is immediately visible and noticeable for both parties compared to normal employment subject to social insurance contributions.

In principle, however, the employer is obliged to pay the U1, U2 and U3 contributions:

- Levy 1 – Continued payment of remuneration in the event of illness: 1 %

- Levy 2 – maternity protection compensation: 0.3 %

- Levy 3 – insolvency money levy: 0.15 %

In total, these levies are only 1.45% of wages. This is very low compared to other forms of employment. This is the main reason why short-term employment is so interesting for both employers and employees.

How much income tax must be paid for short-term employment?

As a short-term employee, no or only low wage taxes – also known as non-wage labor costs – are payable for daily or monthly payroll accounting. The employer is free to decide whether to pay once or monthly. If monthly payroll accounting is chosen, wage tax is calculated on the total monthly wage. The employee’s basic tax-free allowance of €9,000 per year or €750 per year is taken into account.

Example 1 – Employee: in tax class 1 with €600 for the payroll month

If an employee in tax class 1 is paid a gross salary of €600, no income tax has to be paid. The reason for this is that the amount is below the basic monthly tax-free allowance of € 750.

Example 2 – Employee: in tax class 1 with € 1,000 for the payroll month

If an employee in tax class 1 is paid a gross salary of € 1,000, the employee only pays around € 40 in wage tax.

Example 3 – Employee: in tax class 6

If an employee is in tax class 6, the wage tax will increase as the monthly basic allowance of € 750 is not taken into account. This means that the taxable basis and consequently the wage tax will be higher.

Higher wage tax for daily payroll accounting

If payroll accounting is carried out on a daily basis, i.e. payroll accounting is carried out for each individual working day, a different form of taxation is used. In this case, the daily wage is extrapolated to the month. Based on this, a wage tax rate is calculated on the extrapolated monthly wage. In this case, the employee must pay a higher wage tax of between approx. 10% and 30% of the gross wage.

The employee should have agreed the payroll options and tax class with the employer before starting work. This is the only way to avoid disappointment with regard to low net wages.

Is it worth filing an income tax return for short-term employment?

In all cases, it is worth filing an income tax return if an employee was employed and accounted for as a short-term employee.

In principle, income from short-term employment is not tax-free. The employee works via the income tax card. The employer pays the wage tax directly to the tax office as a so-called advance wage tax deduction. The amount is shown on the wage slip and wage tax statement. At the end of the year, the employee can reclaim part or even all of the wage tax from the tax office as part of the income tax return.

If annual income is below the basic tax-free allowance of EUR 9,000, the employee can reclaim the entire wage tax. If the annual income exceeds this threshold, a progressive tax rate is set based on the reported annual income. In short: the higher the annual income, the higher the tax rate.

In the case of daily payroll accounting, the wage tax payment itself is only estimated. A steady income is assumed. However, since the employee only works a few days, the actual tax burden is much lower. This difference can be reclaimed by the employee by filing an income tax return at the end of the year. It is therefore advisable to check and submit an income tax return. Of course, each individual case must be considered individually.

Who is short-term employment suitable for?

Short-term employment was created for seasonal work, e.g. in agriculture. In other words, as the name suggests, the aim is to create a temporary employment relationship. Short-term employment is carried out alongside the actual main job. This means that the employee has a full-time or part-time job or is self-employed. In addition, the status of student, pupil, pensioner or trainee also counts as main employment.

All other professional activities cannot be employed as short-term employment. This is because in these cases it can be assumed that the employment has the character of a main occupation, which is taxable as normal.

| Suitable for … | Not suitable for … |

|

|

Short-term employment is usually very popular with pupils, trainees and students due to the low tax burden. On the one hand, the low tax burden is very attractive. On the other hand, there is also often the time available to pursue additional employment alongside their main occupation.

The 70-day rule

In order to do justice to the nature of temporary additional employment, the legislator has defined a limit on the number of permitted working days per calendar year. Until 2014, only 50 working days were permitted. Since 01.01.2015, however, up to 70 working days per calendar year are permitted.

Each person is therefore only entitled to work 70 days in a calendar year in short-term employment. It does not matter how many employment relationships have been concluded with one or more employers in the form of short-term employment. The total sum of all working days of all employers in short-term employment in the calendar year always counts.

For example, if the employee has already worked 25 working days as a KFB employee with employer A and another 20 days with employer B, the total number of working days as a KFB employee is 45 working days for the employee. Employment such as mini-jobs do not have to be taken into account here. However, working student jobs or voluntary internships must be taken into account.

If the employee exceeds the number of these working days, short-term employment becomes normal employment with full taxation. As a result, the employee and the employer must pay other social security contributions and taxes – even retrospectively. It does not matter whether the employee has concealed employment. It is therefore recommended to record and document the exact working days per calendar year for all employment relationships.

The 3-month rule

In order to further emphasize the character of temporary additional employment, a time limit has also been set. In the case of a 5-day week, an employee may be employed for a maximum of 3 months in the course of short-term employment. If this time limit is exceeded, the employment is considered normal employment.

The regulations clearly show that short-term employment is really only intended for temporary additional income. All other activities are to be assessed as normal main employment.

What is the difference between short-term employment and a mini-job?

In the case of a mini-job – also known as a €520 job – the employee receives a maximum of €520 per month. This can also be for an indefinite period of time. Short-term employment is limited in terms of quantity and duration. The taxation for a mini-job is higher and different compared to short-term employment. Here is an exemplary comparison:

| Short-term employment | Mini job | |

| Legal basis | § Section 8 para. 1 no. 2 SGB IV | § Section 8 (1) no. 1 SGB IV |

| Wage: 30 hours × 14 € | 420,00 € | 420,00 € |

| Social security contributions | 0,00 € | |

| Wage tax according to tax class I | 0,00 € | |

| Flat-rate health and pension insurance – 13 % + 15 % | 117,60 € | |

| Flat-rate wage tax 2% | 8,40 € | |

| Levy U1/U2 and insolvency money levy – 1.1 %, 0.24 %, 0.06 % | 8,14 € | 8,14 € |

| Total amount | 428,14 | 554,14 |

Which income tax class to choose for short-term employment?

The employee can only be billed once per month in income tax class 1 for short-term employment. Any further employment must be in tax class 6. If the information has been incorrectly entered in tax class 1, this is automatically corrected to tax class 6 by the tax offices.

It is also possible for the employee to have a mini-job as well as short-term employment in the same month. However, here too, tax class 1 (or 2, 3 or 4) may only be applied once. All other jobs are then settled in tax class 6.

The exact tax assessment remains separate from the monthly statement in the income tax return. Here, all types of income are added together and the correct annual income tax is calculated.

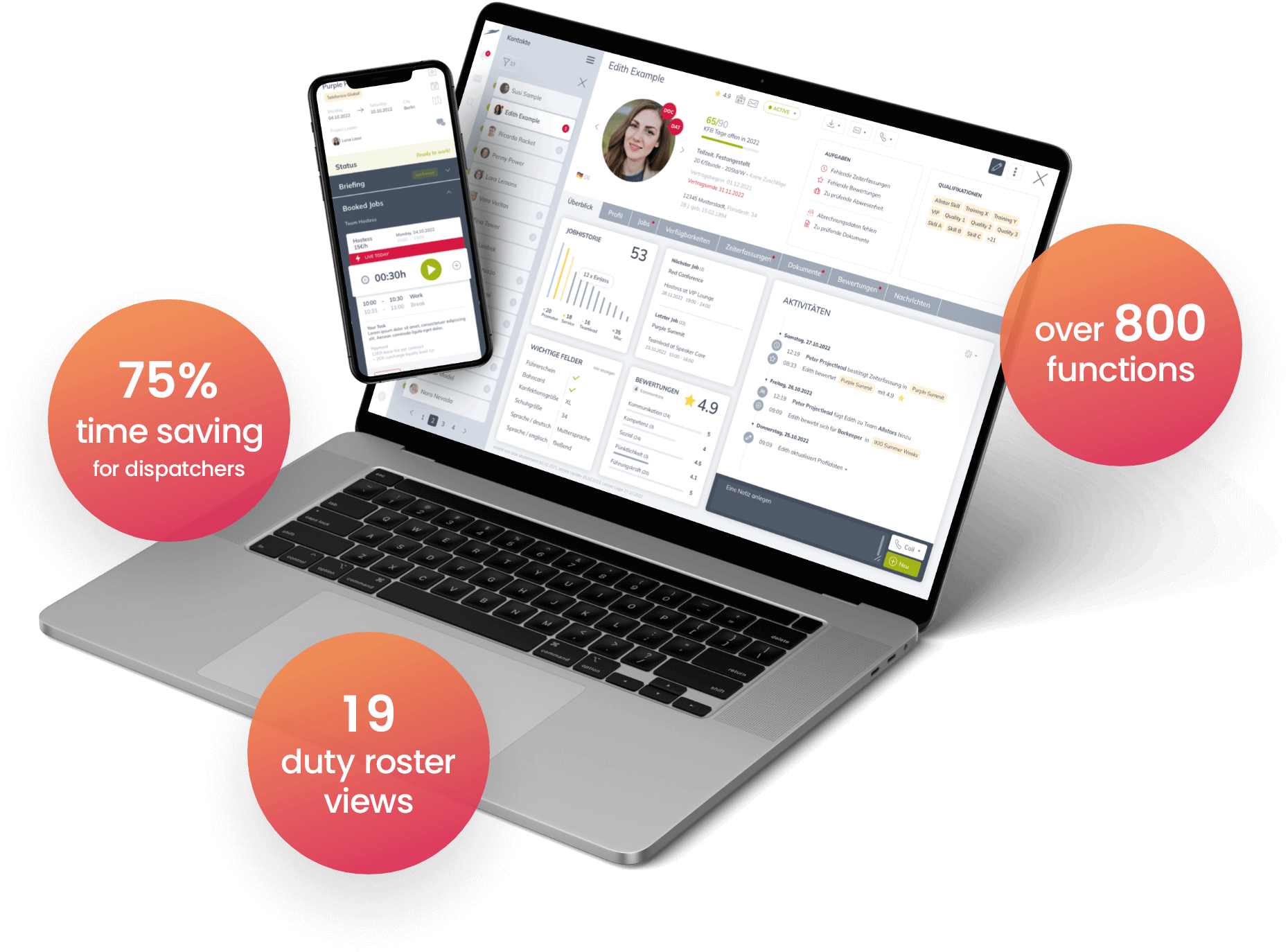

How does Teamhero help with short-term employment?

Short-term employment has some formal framework conditions that must be observed by the employee and the employer. Teamhero helps to comply with these. Among other things, Teamhero can …

- record all personnel master data and track changes.

- calculate the exact daily wage.

- refer to expiring employment contract with 3 month rule.

- indicate that the 70-day rule has been exceeded.

- draw up corresponding employment contracts.

- document the entry and exit date properly.

- Calculate and output the number of tax days.

- output the HR master data and transaction data for common payroll programs such as DATEV LODAS, Sage HR and XLS.

Disclaimer

Please note that the texts on this website and the related contributions are provided for general informational purposes only and do not constitute tax or legal advice in the proper sense. For individual cases, we always recommend seeking specific legal advice tailored to the circumstances of the situation. The information is provided to the best of our knowledge and belief, without any guarantee of accuracy, completeness, or validity.